Despite posting strong double-digit revenue growth and a 41% jump in net profit, Airtel Uganda’s 2025 financial results reveal mounting cost pressures, rising finance charges, and a growing short-term debt burden that could weigh on future performance.

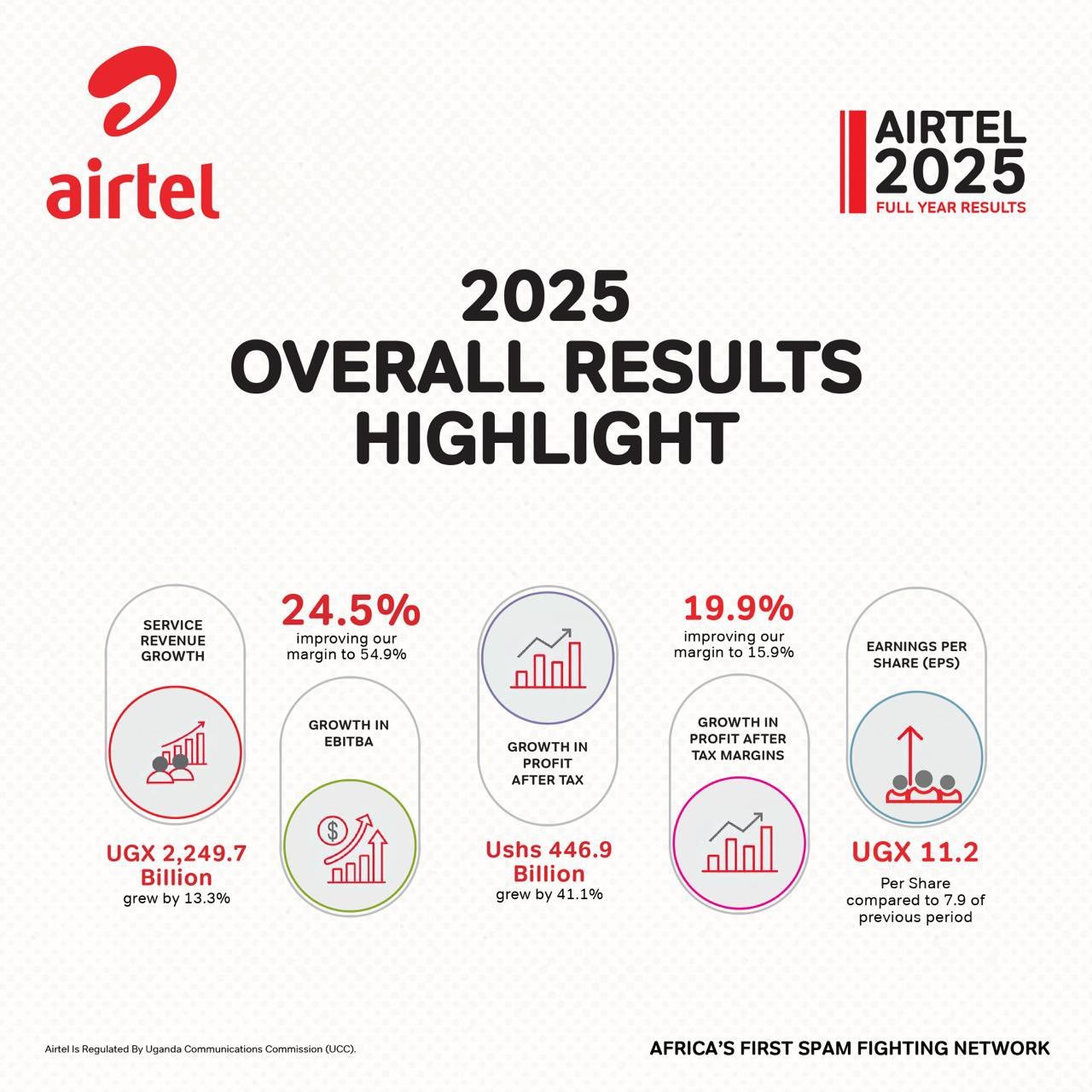

The telecom giant reported revenue of Shs 2.25 trillion for the year ended December 31, 2025 — up 13.3% from Shs 1.99 trillion in 2024.

Profit after tax climbed sharply to Shs 446.9 billion from Shs 316.7 billion the previous year.

However, beneath the headline growth figures, the company’s cost structure and financing profile show areas of concern.

Finance Costs Surge Past Shs 222 Billion

One of the most significant pressure points was finance costs, which jumped to Shs 222.9 billion in 2025 from Shs 192.4 billion in 2024. Net finance charges rose to Shs 209.3 billion, largely driven by interest on lease liabilities.

Lease-related obligations remain substantial, with lease liabilities standing at Shs 1.26 trillion (both current and non-current combined). Interest paid on lease liabilities alone rose sharply to Shs 106.6 billion from Shs 72.2 billion the previous year — a nearly 48% increase.

This highlights Airtel’s heavy reliance on leased infrastructure, which continues to inflate financing costs even as traditional bank borrowings slightly declined overall.

Short-Term Borrowings Increase

Although total market debt reduced marginally from Shs 653.5 billion to Shs 645.0 billion, the composition of that debt shifted in a concerning direction.

Current borrowings rose significantly to Shs 455.4 billion from Shs 394.8 billion, indicating higher short-term repayment pressure. At the same time, non-current borrowings fell to Shs 189.6 billion from Shs 258.7 billion.

This shift suggests more obligations are now falling due within 12 months — tightening liquidity flexibility despite improved operating cash flows.

Network and Marketing Costs Climb

Operating expenses continued to grow across key cost lines:

- Network operating expenses rose to Shs 353.6 billion from Shs 334.1 billion.

- Sales and marketing expenses climbed to Shs 246.7 billion from Shs 227.2 billion.

- Depreciation and amortisation increased to Shs 386.2 billion from Shs 363.3 billion, reflecting continued capital investment, including the addition of 258 new sites.

While operating profit improved to Shs 849.2 billion, these rising costs underscore the increasingly expensive nature of telecom expansion and customer acquisition in a competitive market.

Capital Intensity Remains High

The company spent Shs 229.1 billion on property, plant and equipment during the year, alongside Shs 11.2 billion on intangible assets. Capital work-in-progress also jumped sharply to Shs 88.4 billion from Shs 29.1 billion — signaling ongoing infrastructure commitments that will require continued funding.

Such capital intensity, combined with high lease obligations, means Airtel must sustain strong cash generation to comfortably support expansion.

Heavy Dividend Payouts Drain Cash

Airtel paid out Shs 404 billion in dividends during 2025, up from Shs 301 billion in 2024 — even as it continues to carry significant financing costs and lease liabilities.

Net cash used in financing activities stood at Shs 582.8 billion. Although operating cash flow improved to Shs 1.01 trillion, aggressive dividend payouts reduced retained flexibility.

Negative Cash Position Narrows but Persists

While cash and cash equivalents improved to a negative Shs 159.2 billion from negative Shs 351.7 billion, the company still ended the year in an overdraft position — reflecting continued reliance on short-term facilities.

Tax Burden Increases

Income tax expense rose sharply to Shs 193.0 billion from Shs 135.0 billion, consuming a larger share of earnings as profitability increased.

The Bottom Line

Airtel Uganda’s 2025 results show a company delivering strong revenue and profit growth.

However, rising finance costs, heavy lease obligations, increasing short-term borrowings, high capital expenditure, and aggressive dividend payouts expose underlying financial pressures.

The telecom’s performance in 2026 will likely hinge not just on growing revenue, but on managing financing costs, restructuring debt maturity profiles, and balancing shareholder returns with long-term balance sheet stability.

{kind=link}